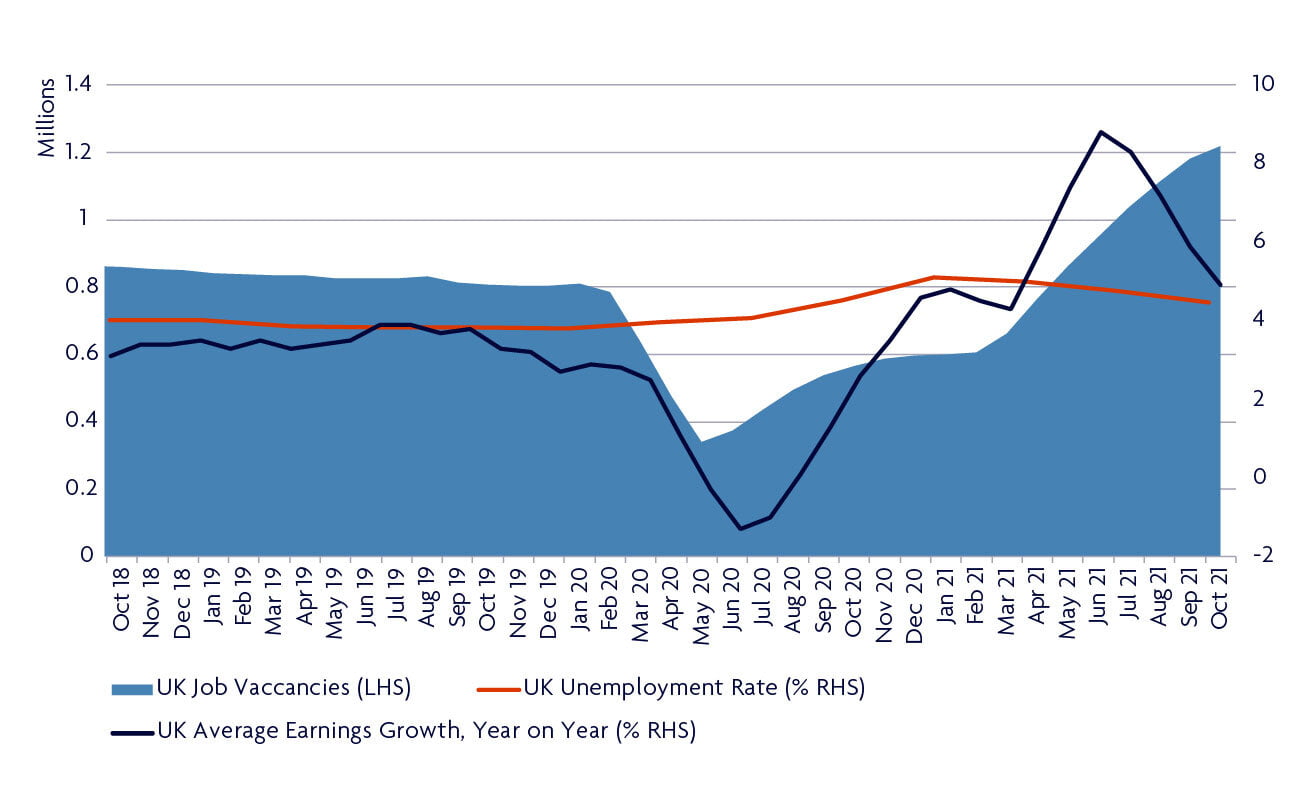

The UK labour market has staged an impressive comeback since the lockdown ended in 2021. Unemployment has remained low, mainly thanks to the furlough scheme, while demand for labour is back to pre-pandemic levels. However, labour shortages abound and the number of job vacancies has topped one million for the first time.

Meanwhile, workers in the US who are wary of catching Covid or have benefited from government stimulus cheques have been reluctant to return to work as the economy opened up last year. Job openings are at record highs and employers are desperate to fill vacancies. The number of Americans quitting their jobs is at the highest on record, with workers taking advantage of the better opportunities available.

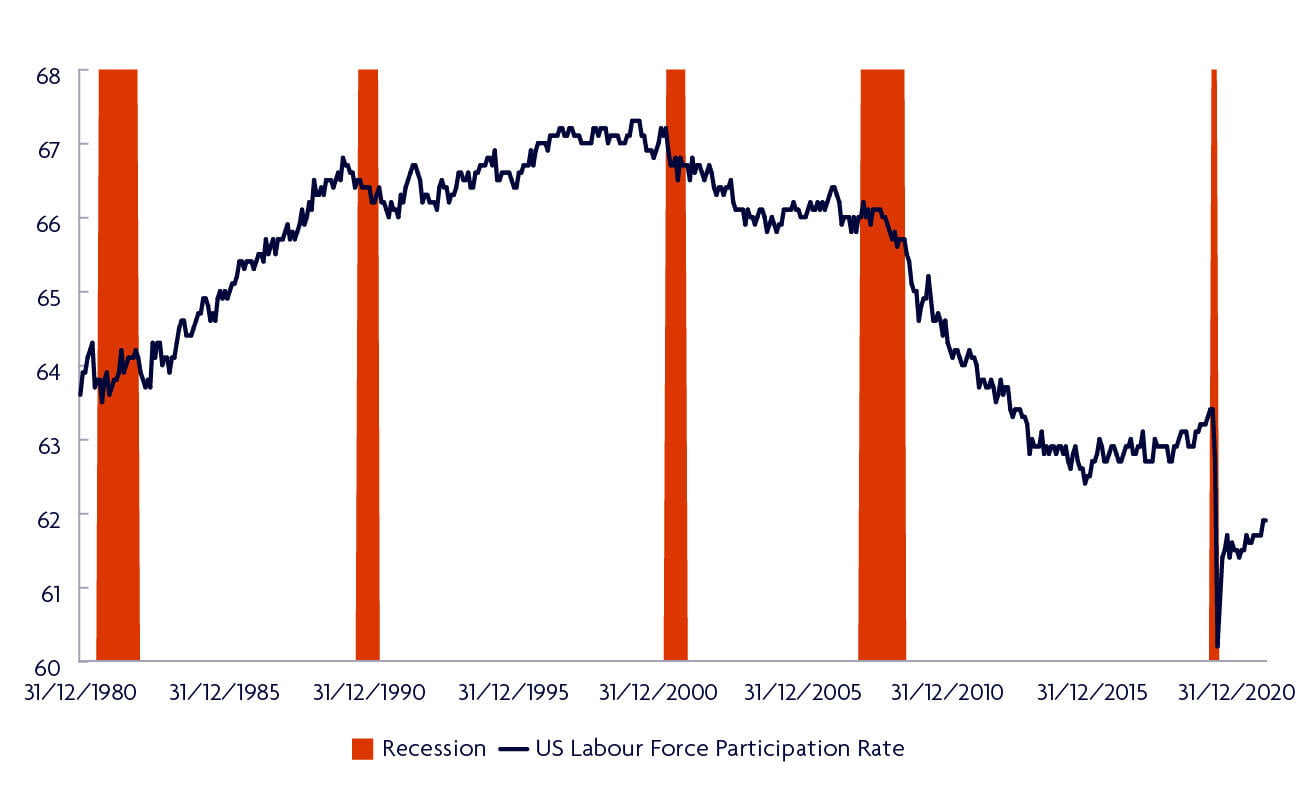

The percentage of working age people who are in the labour force is still well below historical averages and we expect more people to return to work throughout 2022.

Source: Bloomberg. As of 31st December 2021.

Health risks associated with Covid are likely to continue to affect the return to work for front-line workers in sectors like restaurants, bars and retail. At the same time, the value of personal assets for some has increased during the pandemic and as a result many are looking to retire earlier. Meanwhile, people who have been able to amass higher savings may feel they have a buffer, giving them time to wait before rejoining the workforce.

As time progresses, labour participation rates should increase, which is likely to reduce the power employees have to negotiate terms that suit them. While labour shortages have helped to drive up wages, the pace of increase will probably slow as workers return to the labour force.

The trend in of recent months has been that jobs growth has been slowing since last spring. In the spring, restaurants and hospitality generated much of the stronger job growth. By the middle of the year, however, both restaurant sales and payroll levels had nearly reached pre-Covid trends. Meanwhile, the other service sectors hardest hit by Covid restrictions also saw a brief surge in activity in 2021 as restrictions were eased, but these topped out around July as remaining restrictions and consumer fears inhibited further growth.

The manufacturing and construction sectors have recovered strongly and are seeing some further job growth, but nothing like what they experienced in late-2020 and we think growth in these sectors is almost complete. In the remaining service sectors, employment levels are still way below pre-Covid trends so perhaps these other sectors will see better gains in early-2022.

The unemployment rate has fallen as some people have left the labour force, but we expect labour force growth to pick in months to come now that extended unemployment benefits have expired and the holidays are behind us. If this happens, unemployment is likely to rise.

While the effects of the pandemic clearly dominated the higher inflation we saw in 2021, another factor to consider is the impact from the UK’s withdrawal from the European Union. As the fog of the pandemic clears, there are two main ways that we expect the post-Brexit effects on inflation to become clearer.

The first relates to the labour market where a large number of European nationals left the UK during the pandemic. Consider for example a European national that had moved to the UK in recent years, worked in hospitality and lived in rented accommodation. If pandemic rules meant that their job was lost or furloughed and there were heavy restrictions on any social interactions, returning to live with family in their home country would likely be an appealing option. Post-Brexit visa rules make it much more difficult for EU nationals to work in the UK and employers have reported significant difficulties in hiring.

The Bank of England is concerned that the tight labour market will continue to push wages higher, which could combine with the current high headline inflation rates to cause medium and longer-term inflation expectations to become entrenched.

The unemployment rate is relatively low at 4.2%, and there are a record 1.2 million job vacancies (Fig. 4). These factors are likely to continue to exert upward pressure on wage growth, which could combine with the current high inflation to cause medium-term inflation expectations to be stickier than in the US. Against these concerns, in December 2021 the Bank of England became the first G7 central bank to raise interests since the outbreak of the pandemic.

The second challenge is the greater trade frictions post-Brexit. While there are hopes that businesses will adjust to new the new rules and requirements, there are costs associated with doing so and these could feed through into higher consumer prices.

In the UK, the Bank of England expects inflation to peak around 6% in April before falling back in the second half of the year. This could lead to further interest rate hikes later this year and an underperformance of gilts (bonds issued by the UK government). With the labour challenges more pronounced in the UK, this could be a headwind for economic growth and poses challenges for companies exposed to the domestic economy.

In the US, as more workers return to the labour force, we expect inflationary pressures to fade and growth to remain relatively strong, allowing the US Federal Reserve to raise interest rates relatively slowly.

Aside from easing inflationary pressures, people returning to work is good for the economy as they are likely to spend more when they go out – which supports economic growth and would therefore benefit companies exposed to the US economy. In particular, companies in the services and transport sectors, which were most affected by lockdowns, should benefit from this trend .