In 2021 global trade rebounded strongly after the slump caused by the Covid-19 pandemic. The surge in demand for goods combined with disruption to shipping schedules, lack of containers and a shortage of lorry drivers disrupted supply chains and led to shortages of many goods. Bottlenecks were made worse by workers with Covid having to isolate, while the impact of Brexit contributed to problems in the UK.

We have seen early signs of supply chain issues easing and this should continue throughout the year. However, it will take some time to fully unwind. In the meantime, we may go through periods of product shortages in some sectors.

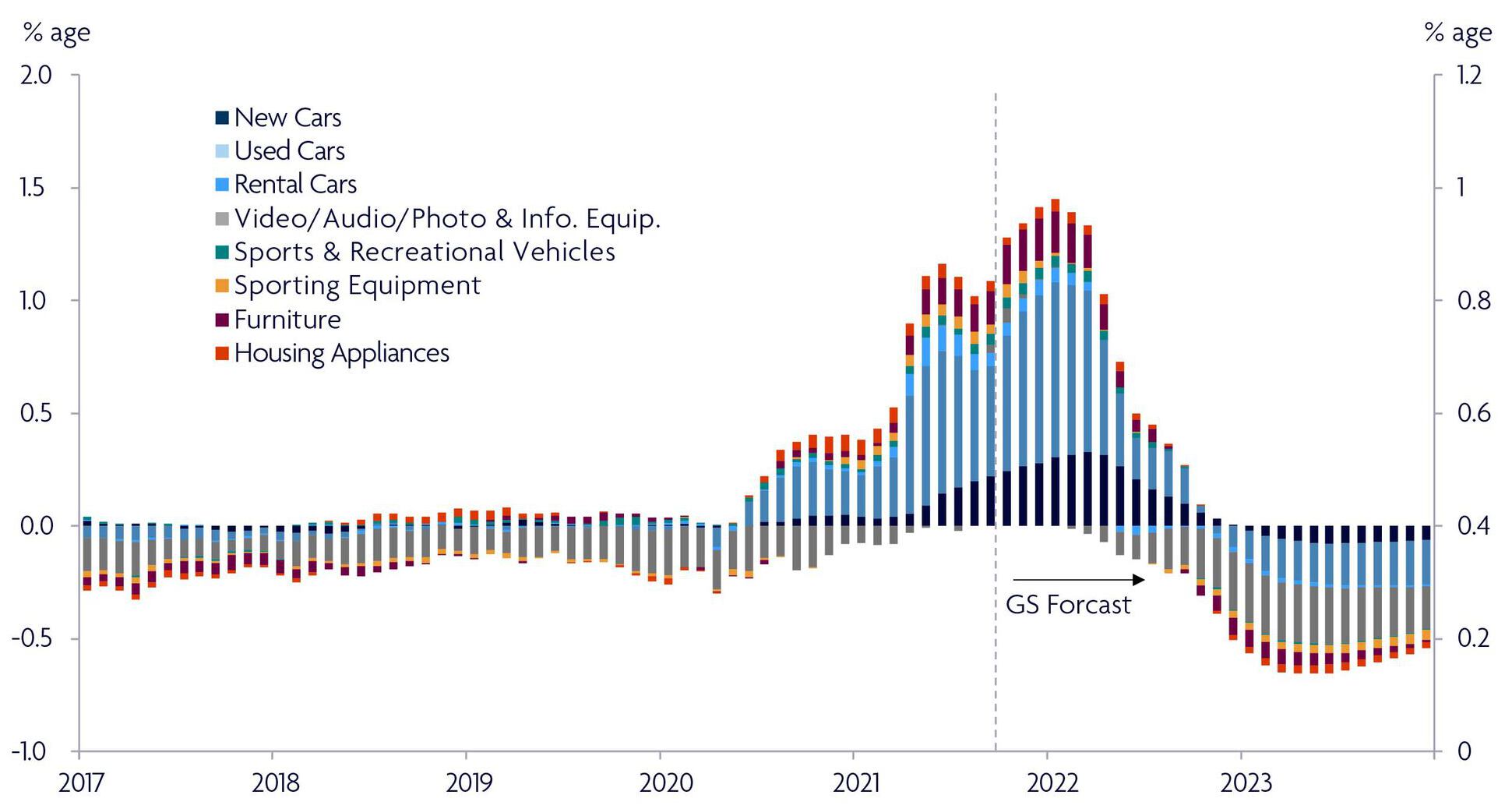

This chart shows the impact that areas exposed to supply chain challenges in 2021 had on inflation. Looking forwards, falling prices for these goods are expected to reduce inflation throughout 2022 and into 2023.

Source: Goldman Sachs

As consumers begin spending more money on services, this should help to ease the pressure on global supply chains. However, there is likely to be sporadic disruption to supply chains in zero-Covid regions, such as China, if workers have to go into lockdown or quarantine. Possible new variants could also pose a risk, albeit a low one, to supply chains if they prove resistant to vaccines and countries have to reintroduce social restrictions.

Hear what Ian Shepherdson, Chief Economist at Pantheon Macroeconomics, has to say on supply chains. Pantheon Macroeconomics is a partner of Omnis and provides us access to economic data and intelligence.

Inflation has rocketed around the world as prices jumped higher due to shortages of products and firms having to pay more for transportation. While inflation is likely to remain elevated in the shorter term, some companies will be in a stronger position than others to pass on higher costs to their customers. In this environment, it is important to actively choose which companies to invest in and which to avoid. For example, companies that have pricing power, such as supermarkets, are likely to pass on higher costs to consumers, thereby protecting their profit margins.

As bottlenecks ease, inflation should start to moderate. If inflation falls and global growth slows as we expect, central banks are unlikely to increase interest rates too much in 2022. We expect only a moderate hike to interest rates across the world, which would be positive for growth companies, such as those in the technology sector. Our investment managers actively invest in companies with sound fundamentals that can navigate supply chain issues.

Here are some thoughts from Fidelity International, who currently manager the Omnis Global Emerging Markets Equity Leaders Fund, the Omnis European Equity Leaders Fund and the Omnis Strategic Bond Fund. Overall, there is a mixed global picture on supply chain issues due to pressures from freight and supply chain issues. The majority of our analysts are expecting costs to rise, but also suggest that pressures could be easing slightly. Analysts still expect shortages to bite into some companies’ earnings and margins in 2022.

Port congestion across both North America and Europe remains at record levels with little signs of improvement, resulting in very high freight rates. Due to the strong consumer demand environment, product shortages were common during the most recent Christmas period. We are hopeful that these challenges will fade, but our industrials analysts have not seen particularly strong evidence of supply chains easing yet and it’s possible issues continue throughout the year.

Supply chain disruptions predominately relate to logistical challenges and we have seen some companies that used middleman freight suppliers shifting to direct contracts with shipping companies over the recent months in order to save costs and have better visibility.

Within India, for example, we are witnessing some easing in supply chain problems in areas like Autos and Chemicals. Companies like Maruti and Eicher motors are now close to returning to more normal production levels. In areas like Pharmaceuticals and Chemicals, whilst availability of raw material has improved, prices remain elevated.